Nomi Prins writes about bailouts in the time of the coronavirus.

Wall Street, Nov. 21, 2009. (Dave Center, Flickr)

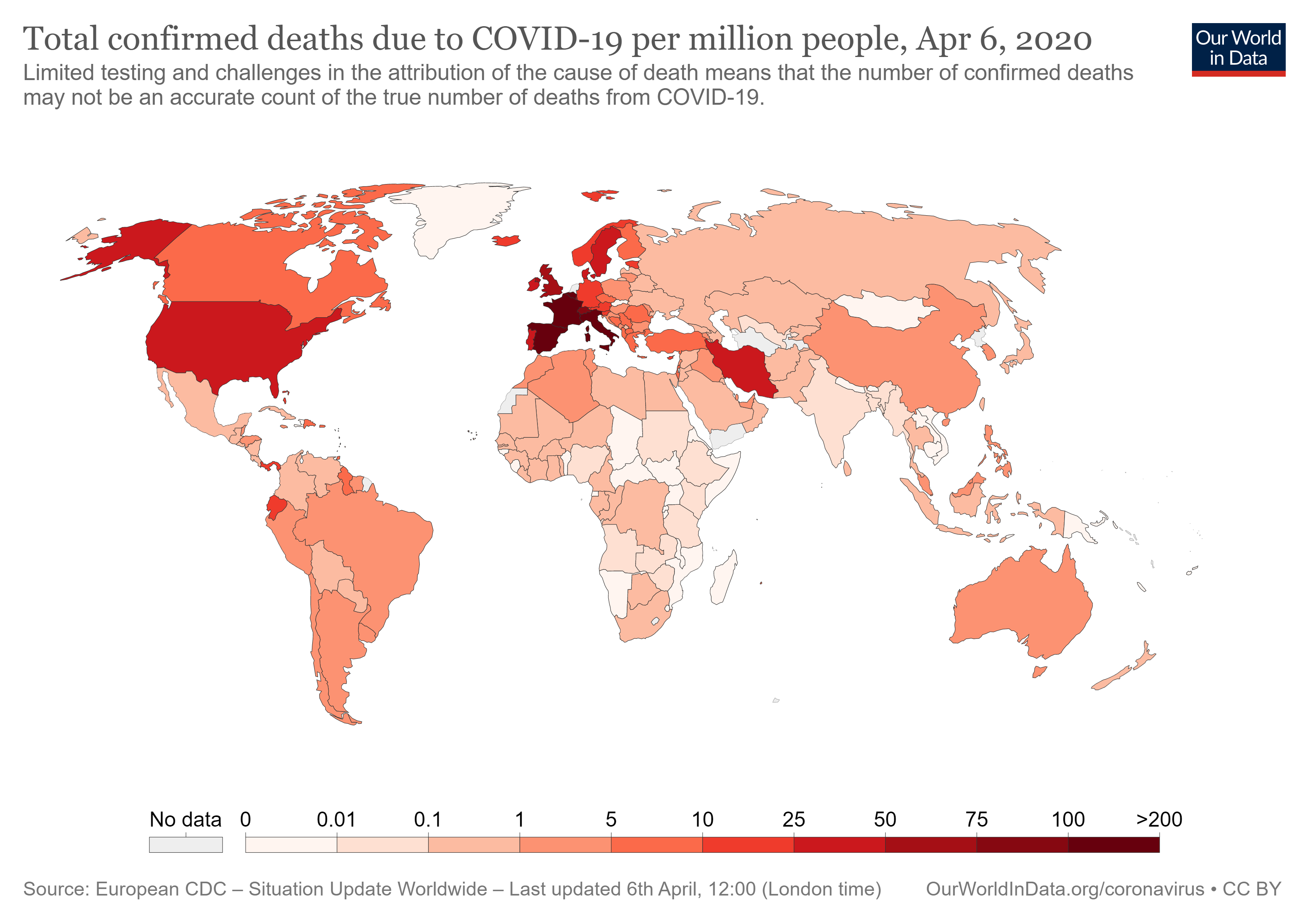

To say that these are unprecedented times would be the understatement of the century. Even as the United States became the latest target of Hurricane Covid-19, in “hot spots” around the globe a continuing frenzy of health concerns represented yet another drop down the economic rabbit hole.

To say that these are unprecedented times would be the understatement of the century. Even as the United States became the latest target of Hurricane Covid-19, in “hot spots” around the globe a continuing frenzy of health concerns represented yet another drop down the economic rabbit hole.

Stay-at-home orders have engulfed the planet, encompassing a majority of Americans, all of India, the United Kingdom, and much of Europe. A second round of cases may be starting to surface in China. Meanwhile, small- and medium-sized businesses, not to speak of giant corporate entities, are already facing severe financial pain.

I was in New York City on 9/11 and for the weeks that followed. At first, there was a sense of overriding panic about the possibility of more attacks, while the air was still thick with smoke. A startling number of lives were lost and we all did feel that we had indeed been changed forever.

Nonetheless, the shock was momentary. Small businesses, even in the neighborhood of the Twin Towers, reopened quickly enough while, in the midst of psychic chaos, President George W. Bush urged Americans to continue to fly, shop, and even go to Disney World.

Think of the coronavirus, then, as a different kind of 9/11. After all, the airlines are all but grounded, restaurants and so many other shops closed, Disney World shut tight, and the death toll is already well past that of 9/11 and multiplying fast. The concept of “social distancing” has become omnipresent, while hospitals are overwhelmed and medical professionals stretched thin. Pandemic containment efforts have put the global economy on hold. This time, we will be changed forever.

(Our World in Data, CC BY 4.0, Wikimedia Commons)

Figures on job cuts and business closures could soon eclipse those from the aftermath of the financial collapse of 2008. The U.S. jobless rate could hit 30 percent in the second quarter of 2020, according to Federal Reserve Bank of St. Louis President James Bullard, which would mean that we’re talking levels of unemployment not seen since the Great Depression of the 1930s. Many small companies will be unable to reopen. Others could default on their debts and enter bankruptcy.

After all, about half of all small businesses in this country had less than a month’s worth of cash set aside as the coronavirus hit and they employ almost half of the private workforce. In truth, mom-and-pop stores, not the giant corporate entities, are the engine of the economy. The restaurant industry alone could lose 7.4 million jobs, while tourism and retail sectors will experience significant turmoil for months, if not years, to come.

In the first week of coronavirus economic shock, a record 3.3 million Americans filed claims for unemployment. That figure was nearly three times the peak of the 2008 recession and it doubled to 6.6 million a week later, with future numbers expected to rise staggeringly higher.

As sobering as those numbers were, Treasury Secretary Steve “Foreclosure King” Mnuchin branded them “not relevant.” Tone-deafness aside, the reality is that it will take months, once the impact of the coronavirus subsides, for many people to return to work. There will be jobs and possibly even sub-sectors of the economy that won’t rematerialize.

This cataclysm prompted Congress to pass the largest fiscal relief package in its history. As necessary as it was, that massive spending bill was also a reminder that the urge to offer corporations mega-welfare not available to ordinary citizens remains a distinctly all-American phenomenon.

Reflections from 2008 Financial Crisis

The catalyst for this crisis is obviously in a different league from that of 2008, since a viral pandemic is hardly nature’s equivalent of a subprime meltdown. But with an economic system already on the brink of crashing, one thing will prove similar: instability for a vulnerable majority is likely to be matched by nearly unlimited access to money for financial elites who, with stupendous subsidies, will thrive no matter who else goes down.

Once the virus recedes, stock and debt bubbles inflated over the past 12 years are likely to begin to grow again, fueled as then by central bank policies and federal favoritism. In other words, we’ve seen this movie before, but call the sequel: Contagion Meets Wall Street.

Secretary of the Treasury Steven Mnuchin discusses Covid-19 stimulus package, March 25, 2020. (White House, Tia Dufour)

Unlike in 2020, in the early days of the 2008 financial crisis, economic fallout spread far more slowly. Between mid-September of that year when Lehman Brothers went bankrupt and October 3rd, when the Troubled Asset Relief Program, including a $700 billion Wall Street and corporate bailout package, was passed by Congress, banks were freaked out by the enormity of their own bad bets.

Yet no one then should have been surprised, as I and others had been reporting that the amount of leverage, or debt, in the financial system was a genuine danger, especially given all those toxic subprime mortgage assets the banks had created and then bet on. After Bear Stearns went bankrupt in March 2008 because it had borrowed far too much from other big banks to squander on toxic mortgage assets, I assured listeners on Democracy Now! that this was just the beginning — and so it proved to be. Taxpayers would end up guaranteeing JPMorgan Chase’s buyout of Bear Stearns’s business and yet more bailouts would follow — and not just from the government.

Leaders of the Federal Reserve would similarly provide trillions of dollars in loans, cheap money, and bond-buying programs to the financial system. And this would dwarf the government stimulus packages under both George W. Bush and Barack Obama that were meant for ordinary people.

As I wrote in “It Takes a Pillage: An Epic Tale of Power, Deceit, and Untold Trillions,” instead of the Fed buying those trillions of dollars of toxic assets from banks that could no longer sell them anywhere else, it would have been cheaper to directly cover subprime mortgage payments for a set period of time. In that way, people might have kept their homes and the economic fallout would have been largely contained. Thanks to Washington’s predisposition to offer corporate welfare, that didn’t happen — and it’s not happening now either.

None of this is that complicated: when a system is steeped in so much debt that companies can’t make even low-rate debt payments and have insufficient savings for emergencies, they can crash — fast. All of this was largely forgotten, however, as a combination of Wall Street maneuvering, record-breaking corporate buybacks, and ultra-low interest rates in the years since the financial crisis lifted stock markets globally.

Below the surface, however, an epic debt bubble was once again growing, fostered in part by record corporate debt levels. In 2009, as the economy was just beginning to show the first signs of emerging from the Great Recession, the average American company owed $2 of debt for every $1 it earned. Fast forward to today and that ratio is about $3 to $1. For some companies, it’s as high as $15 to $1. For Boeing, the second largest recipient of federal funding in this country, it’s $37 to $1.

What that meant was simple enough: anything that disrupted the system was going to be exponentially devastating. Enter the coronavirus, which is now creating a perfect storm on Wall Street that’s guaranteed to ripple through Main Street.

Trillions on the Line

President Donald Trump surrounded by advisers during $2.2 trillion CARES Act signing. (White House, Shealah Craighead)

In total, the CARES Act that Congress passed offers about $2.2 trillion in government relief. As President Donald Trump noted while signing the bill into law, however, total government coronavirus aid could, in the end, reach $6.2 trillion. That’s a staggering sum. Unfortunately, you won’t be surprised to learn that, given both the Trump administration and the Fed, the story hardly ends there.

More than $4 trillion of that estimate is predicated on using $454 billion of CARES Act money to back Federal Reserve-based corporate loans. The Fed has the magical power to leverage, or multiply, money it receives from the Treasury up to 10 times over. In the end, according to the president, that could mean $4.5 trillion in support for big banks and corporate entities versus something like $1.4 trillion for regular Americans, small businesses, hospitals, and local and state governments. That 3.5 to 1 ratio signals that, as in 2008, the Treasury and the Fed are focused on big banks and large corporations, not everyday Americans.

In addition to slashing interest rates to zero, the Fed announced a slew of initiatives to pump money (“liquidity”) into the system. In total, its life-support programs are aimed primarily at banks, large companies, and markets, with some spillage into small businesses and municipalities.

Its arsenal consists of $1.5 trillion in short-term loans to banks and an alphabet soup of other perks and programs. On March 15th, for instance, the Fed announced that it would restart its quantitative easing, or QE, program. In this way, the U.S. central bank creates money electronically that it can use to buy bonds from banks. In an effort to keep Wall Street buzzing, its initial QE revamp will enable it to buy up to $500 billion in Treasury bonds and $200 billion in mortgage-backed securities — and that was just a beginning.

Two days later, the Fed created a Commercial Paper Funding Facility through which it will provide yet more short-term loans for banks and corporations, while also dusting off its Term Asset-Backed Securities Loan Facility (TALF) to allow it to buy securities backed by student loans, auto loans, and credit-card loans. TALF will receive $10 billion in initial funding from the Treasury Department’s Emergency Stabilization Fund (ESF).

And there’s more. The Fed has selected asset-management goliath BlackRock to manage its buying programs (for a fee, of course), including its commercial mortgage and two corporate bond-buying ones (each of which is to get $10 billion in seed money from the Treasury Department’s ESF). BlackRock will also be able to purchase corporate bonds through various Exchange Traded Funds, of which that company just happens to be the biggest provider.

Surpassing measures used in the 2008 crisis, on March 23, the Fed said it would continue buying Treasury securities and mortgage-backed securities “in the amounts needed to support smooth market functioning.” In other words, unlimited quantitative easing. As its chairman, Jerome Powell, told the “Today Show,” “When it comes to this lending, we’re not going to run out of ammunition, that doesn’t happen.” In other words, the Fed will be dishing out money like it’s going out of style — but not to real people.

By March 25, the Fed’s balance sheet had already surged to $5.25 trillion, larger than at its height — $4.5 trillion — in the aftermath of the global financial crisis and it won’t stop there. In other words, the 2008 playbook is unfolding again, just more quickly and on an even larger scale, distributing a disproportionate amount of money to the top tiers of the business world and using government funds to make that money stretch even further.

Members of West Virginia National Guard assist with Covid-19 testing at a Charleston nursing home, April 6, 2020. (U.S. Army, Edwin L. Wriston)

Relief Package for Whom?

By now, in our unique pandemic moment, something seems all too familiar. As in 2008, the most beneficial policies and funding will be heading for Wall Street banks and behemoth corporations. Far less will be going directly to American workers through tangible grants, cheaper loans, or any form of debt forgiveness. Even the six months of student-loan payment relief (only for federal loans, not private ones) just pushes those payments down the road.

The historic $2.2 trillion coronavirus relief package is heavily corporate-focused. For starters, a quarter of it, $500 billion, goes to large corporations. At least $454 billion of that will back funding for up to $4.5 trillion in corporate loans from the Fed and the remainder will be for direct Treasury loans to big companies. Who gets what will be largely Treasury Secretary Mnuchin’s choice. And mind you, we may never know the details since President Trump is committed to making this selection process as non-transparent as possible.

There’s an additional $50 billion that’s to be dedicated to the airline industry, $25 billion of which will be in direct grants to airlines that don’t place employees on involuntary furlough or discontinue flight service at airports through September. Right after the bill passed, the airline industry announced that more workforce cuts are ahead (once it gets the money).

Another $17 billion is meant for “businesses critical to maintaining national security,” one of which could eventually be White House darling Boeing. There’s also a corporate tax credit worth about $290 billon to corporations that keep people on their payrolls and can prove losses of 50 percent of their pre-coronavirus revenue.

More than $370 billion of that congressional relief package will go into Small Business Administration loans meant to cover existing loans and operating and payroll costs as well. Yet receiving such loans will involve a byzantine process for desperate small outfits. Meanwhile, the big banks will get a cut for administering them.

About $150 billion is pegged for the healthcare industry, including $100 billion in grants to hospitals working on the frontlines of the coronavirus crisis and other funds to jumpstart the production of desperately needed (and long overdue) medical products for doctors, nurses, and pandemic patients. Another $27 billion is being allocated for vaccines and stockpiles of medical supplies.

An extra $150 billion will go to cities and states to prop up budgets already over-stretched and in trouble. Those on unemployment benefits will get an increase of $600 per week for four months in a $260 billion unemployment expansion.

Ultimately, however, the relief promised will not cover the basic needs of the majority of bereft Americans. With Main Street’s economy sinking right now, it won’t arrive fast enough either. In addition, the highly publicized part of Congress’s relief package that promises up to $1,200 per person, $2,400 per family, and $500 per child, will be barely enough to cover a month of rent and utilities, let alone other essentials, for the typical working family when it finally arrives. Since disbursement will be based on information the Internal Revenue Service has on each individual and family, if you haven’t filed tax returns in the last year or so or if you filed them by mail, funds could be slower to arrive — and don’t forget that the IRS is facing coronavirus-based workforce challenges of its own.

Best Offense Is a Good Defense

The global economic freeze caused by the coronavirus has crushed more people in a shorter span of time than any crisis in memory. Working people will need far more relief than in the last meltdown to keep not just themselves but the very foundations of the global economy going.

The only true avenue for such support is national governments. Central banks remain the dealers of choice for addicted big corporations, private banks, and markets. In other words, given congressional (and Trumpian) sponsored bailouts and practically unlimited access to money from the Fed, Wall Street will, in the end, be fine.

If ground-up solutions to help ordinary Americans and small businesses aren’t adopted in a far grander way, one thing is predictable: once this crisis has been “managed,” we’ll be set up for a larger one in an even more disparate world. When the clouds from the coronavirus storm dissipate, those bailouts and all the corporate deregulation now underway will have created bank and corporate debt bubbles that are even larger than before.

The real economic lesson to be drawn from this crisis should be (but won’t be) that the best offense is a good defense. Exiting this self-induced recession or depression into anything but a less equal world would require genuine infrastructure investment and planning. That would mean focusing post-relief efforts on producing better hospitals, public transportation networks, research and development, schools, and far more adequate homeless shelters.

In other words, actions offering greater protection to the majority of the population would restart the economy in a truly sustainable fashion, while bringing back both jobs and confidence. But that, in turn, would involve a bold and courageous political response providing genuine and proportionate stimulus for people. Unfortunately, given Washington’s 1-percent tilt and Donald Trump’s CEO empathy, that is at present inconceivable.

Nomi Prins, a former Wall Street executive, is a TomDispatch regular. Her latest book is “Collusion: How Central Bankers Rigged the World.” She is also the author of “All the Presidents’ Bankers: The Hidden Alliances That Drive American Power” and five other books. Special thanks go to researcher Craig Wilson for his superb work on this piece.

This article is from TomDispatch.com.

The views expressed are solely those of the author and may or may not reflect those of Consortium News.

Please Donate to Consortium News.

Before commenting please read Robert Parry’s Comment Policy. Allegations unsupported by facts, gross or misleading factual errors and ad hominem attacks, and abusive or rude language toward other commenters or our writers will not be published. If your comment does not immediately appear, please be patient as it is manually reviewed. For security reasons, please refrain from inserting links in your comments, which should not be longer than 300 words.

The quantitative greasing of the cronies begins again and it is not even half of it as the author details.

People lining up at unemployment offices is not only dumb it is dangerous as they may get the virus. Instead they should be lining up at the drive-up window of the closest bank. Proffering a couple of paycheck stubs would get the unemployed the $1,200 and 1st $600 unemployment check. That is not enough as the author notes. It would put a few crumbs on the table.

A better and quicker solution would be to increase the value of all credit and debit cards by $5000, just for openers. It can be done immediately if the government wants to do something meaningful.

Some banks have a drive-up window for businesses. Small business owners should be in that line. Proffering a business license would render the needed loan. The government can do it right now if it really wants to help.

Like the man said – it ain’t rocket science.

The banks are not going to get hurt. The government always bails out the banks. The only rational basis for giving “money” to banks is so they can pass it on to the people usually demeaned and disparaged as consumers but who are if fact the profit providers in this corrupt oligarchic system.

Excellent article written by someone who understands macroeconomics and central banking. I have some slight quibbles of differences of opinion on some details, but that doesn’t mean that I am right. Maybe…but maybe not. For the most part though, I am in agreement.

As long as people remain willfully ignorant of history and believe the state propaganda put out by K-12, Universities, TV, Hollywood, and “NYT Bestsellers,” Wall Street which controls it all, will always win.

Now some quotes you probably never heard of from major historical figures. More in the “Conspiracy Facts” section of my website, with original sources linked.

“The few who can understand the system (check money and credits) will either be so interested in its profits, or so dependent on its favors, that there will be no opposition from that class, while on the other hand, the great body of the people mentally incapable of comprehending the tremendous advantage that capital derives from the system, will bear its burdens without complaint, and perhaps without even suspecting that the system is inimical to their interests.”

? From a letter written by the Rothschild Bros, of London, England, to a New York firm of bankers, June 26, 1863, from National Economy and Banking System of the United States, by Robert Latham Owen, p. 99-100, presented in Congress on January 24, 1939

“Those who stand ready to furnish this money, are the real rulers. It is so in Europe, and it is so in this country (the US). In Europe, the nominal rulers, the emperors and kings and parliaments, are anything but the real rulers of their respective countries. They are little or nothing else than mere tools, employed by the wealthy to rob, enslave, and (if need be) murder those who have less wealth, or none at all. The Rothschilds, and that class of money-lenders of whom they are the representatives and agents…stand ready, at all times, to lend money in unlimited amounts to those robbers and murderers, who call themselves governments, to be expended in shooting down those who do not submit quietly to being robbed and enslaved.”

? Lysander Spooner, No Treason No VI: The Constitution of No Authority, p. 48, 1867

“We shall have world government, whether or not we like it. The question is only whether world government will be achieved by consent or by conquest.”

? James Paul Warburg, Federal Reserve Chairman and son of Paul Warburg, Federal Reserve Founder, before the Senate Subcommittee on Revision of the United Nations Charter in 1950, February 17, 1950

“Place the money power in the hands of a single individual, or a combination of individuals, and they, by expanding and contracting the currency, may rise or sink prices at pleasure; and by purchasing when at the greatest depression, and selling at the greatest elevation, may command the whole property and industry of the community and control its fiscal operations. The banking system concentrates and places this power in the hands of those who control it, and its force increases just in proportion as it dispenses with a metallic basis. Never was an engine invented better calculated to place the destiny of the many in the hands of the few, or less favorable to that equality and independence which lies at the bottom of our free institutions.”

? John C. Calhoun, 7th Vice President of the USA, 1834, Speeches of John C. Calhoun, p. 281, 1843

“When the Federal Reserve Act was passed, the people of these United States did not perceive that a world banking system was being set up here. A super-state controlled by international bankers and industrialists acting together to enslave the world for their own pleasure. Every effort has been made by the Fed to conceal its powers but the truth is—the Fed has usurped the government. It controls everything here and it controls all our foreign relations. It makes and breaks governments at will.”

? Congressman Louis McFadden, The Unseen Hand, p. 182, 1985

“The bank, Mr. Van Buren is trying to kill me, but I will kill it!”

— Andrew Jackson, 7th US President and only President ever to pay off the National Debt, Autobiography of Martin Van Buren Vol. II, p. 625, 1920

“Throughout the ages it has been the favorite device of the creditor class first to work a contraction of the currency, which bankrupted the debtors, and then to cause inflation which created a rise when they sold the property which they had impounded.”

? Brooks Adams, great grandson of 2nd US President John Adams

“The combination of these two trends – declining real wages and inflated asset prices – led the American middle class to use debt as a substitute of income. People lacked adequate earnings but felt wealthier. A generation of Americans grew accustomed to borrowing against their homes to finance consumption, and banks were more than happy to be their enablers. In my generation, second mortgages were considered highly risky for homeowners. The financial industry re-branded them as home equity loans, and they became ubiquitous. Third mortgages, even riskier, were marketed as ‘home equity lines of credit.”

— Robert Kuttner, American Journalist and Writer

“I am one of those who do not consider a national debt a national blessing, but rather a curse to a republic, inasmuch as it is calculated to raise around the administration a moneyed aristocracy dangerous to the liberties of the country.”

— Andrew Jackson

“All the perplexities, confusion and distress in America arise, not from defects in their Constitution or Confederation, not from want of honor or virtue, so much as from the downright ignorance of the nature of coin, credit and circulation.”

— John Adams, 2nd US President, Letter to Thomas Jefferson, August 25, 1787

I am self-employed with no employees. So is my wife. We are completely without income and have minimal savings. We don’t qualify for unemployment or other assistance. We filed an SBA relief application and didn’t even get a confirmation of the filing.

Meanwhile trillions are poured into giant corporations that have been fleecing everybody for years. Interest rates have been lowered to make even more free money available to banks. Trump has not allowed Disaster Unemployment Assistance that would allow the self-employed to collect unemployment in Federal disaster areas.

Meanwhile the bills keep rolling in. Verizon increased the amount of data on our phone account, laughable because we don’t ever use it. The mortgage bank (not one of the behemoth corporate thieves) waived payments for three months by extending the loan period without penalty and interest. Optimum has offered nothing and in fact recently raised internet connection fees 25%. Discover Card waived the current month’s interest after a phone call. Next month I’ll try again.

If you’re having trouble economically, call and see what – if anything – the corporate vampires will do for you because the government has completely failed. As if that wee news …

I wish I had more and better advice to share. Good luck to all.